Binance.US Updates its Service Terms and Halts USD Withdrawals

- Binance.US said its users’ assets are no longer FDIC-insured.

- Binance.US advised customers to convert their assets to stablecoins or other cryptocurrencies to withdraw them.

- Binance recently announced that it would no longer accept new UK customers.

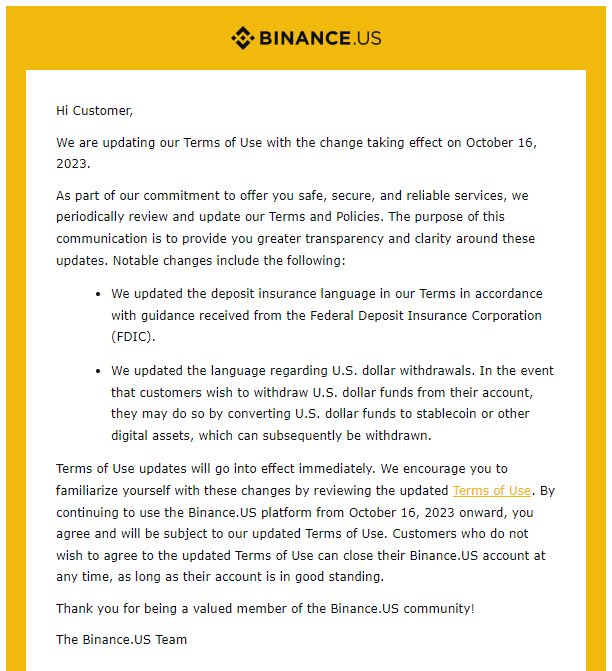

Crypto exchange Binance.US has made changes to its terms of service, suggesting that it will no longer allow direct withdrawals in US dollars. Binance.US made the alleged update on Monday, October 16, and some users have confirmed the change of terms on X (formerly Twitter).

According to a Binance email:

In the event that customers wish to withdraw U.S. dollar funds from their account, they may do so by converting U.S. dollar funds to stablecoin or other digital assets, which can subsequently be withdrawn.

The crypto exchange halted dollar deposits in early June, citing banking partners’ reluctance to interact with the cryptocurrency space as a result of the U.S. Securities and Exchange Commission’s (SEC) “extremely aggressive and intimidating tactics” against the industry.

In its Monday email to users, Binance.US also informed customers that their crypto holdings are no longer FDIC-insured. The crypto exchange said the changes to its terms were done under the FDIC’s guidance. The updated terms now read, “Your accounts and digital assets are not eligible for FDIC insurance protections.”

In 2019, Binance.US claimed its customers’ accounts were insured up to $250,000. The exchange has since deleted the post. At the time, the post stated, “All USD deposits are held in pooled custodial accounts at multiple banks that are insured by the FDIC. The pooled custodial accounts are maintained in a manner that provides access to pass-through FDIC insurance coverage up to the depositor coverage limit, which is currently $250,000.”

The Federal Deposit Insurance Corporation (FDIC) is a US agency that protects US citizens from losing up to a certain amount of their money in the case of a bank collapse. The FDIC recently warned US users that funds deposited with a “crypto-based financial services provider” are neither safeguarded nor insured by the FDIC.

The FDIC said in a statement:

Know that crypto deposits are not FDIC-insured, period. If something happens, the government may not have an obligation to step in and help get your money back.

In a separate case, the Federal Trade Commission (FTC) accused Stephen Ehrlich, the former CEO of the defunct cryptocurrency broker Voyager Digital, of making a fraudulent claim that customer accounts were protected by the FDIC. Ehrlich was also accused by the Commodities and Futures Trading Commission (CFTC) of fraud and failing to register his company’s services.

Ehrlich joins the growing list of crypto founders prosecuted by US regulators. FTX founder Sam Bankman-Fried and Celsius’ Alex Mashinsky are two other prominent crypto founders charged by US prosecutors.

Authorities claim that these cases reflect the need for rules governing the crypto sector.

Lawrence has covered some exciting stories in his career as a journalist, he finds blockchain-related stories very intriguing. He believes Web3 will change the world and wants everyone to be a part of it.